Depreciable Life Carpet Rental Property

Depreciable Life Life Expectancy For Rental Purchases

A Landlord Inventory Template Is A List Of Everything That Your Landlord Provides With The Property You Rent For Example Being A Landlord Words Word Template

2018 Tax Laws That Affect Real Estate We Will Guide You Through The Sales Process Consult Your Cpa For Det Investment Property Estate Tax Real Estate

How The New Tax Law Affects Rental Real Estate Owners

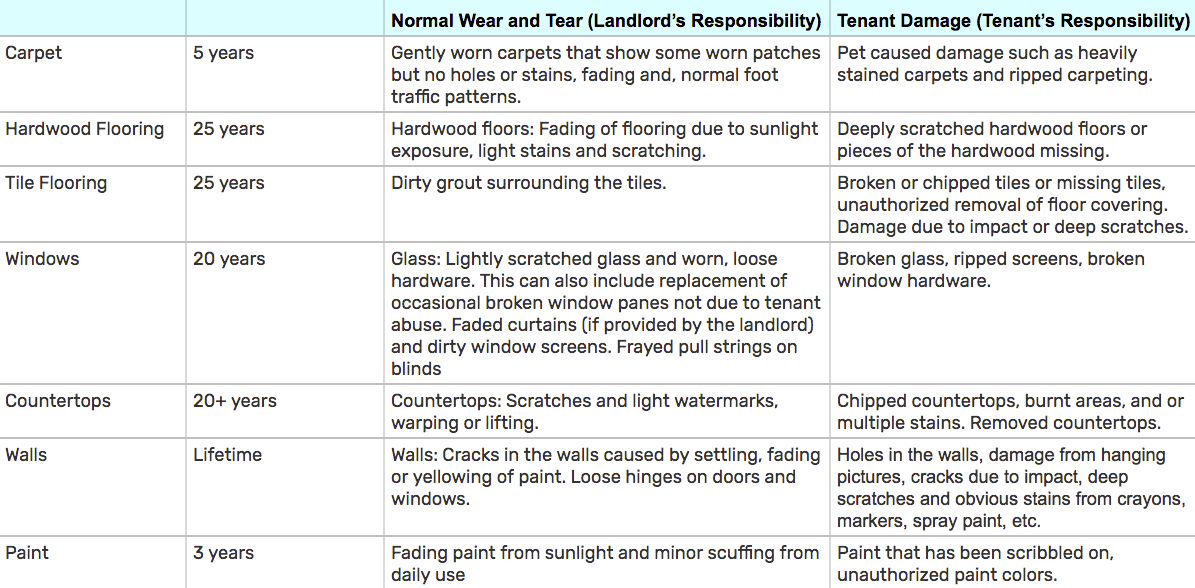

What Is Considered Normal Wear And Tear Lambert Investments Inc

Everything You Need To Know About Depreciation On Rental Property Investment Property Tips Mashvisor Real Estate Blog

When using a nonrecovery method the life or class life is a mandatory entry.

Depreciable life carpet rental property.

Publication 527 Residential Rental Property Depreciation

Depreciation Recapture What Is It And How Can I Reduce It

Inventory Template For Furnished Rental Property Word Template Budget Spreadsheet Template Being A Landlord

Publication 527 Residential Rental Property Rental Expenses

What If You Forgot To Depreciate Your Rental Property Ipropertymanagement Com

A Landlord Inventory Template Is A List Of Everything That Your Landlord Provides With The Property You Rent Being A Landlord Free Word Document Word Template

How To Calculate Depreciation Expense For Business

How To Deduct Rental Property Depreciation Wealthfit

What Is Rental Property Depreciation And How Does It Work

Rental Property Depreciation Reducing Your Tax Burden 37parallel Com

Uwqtkgr1p2qqum

Residential Rental Property Depreciation Calculator

A In Depth Review Of The Best Tax Deductions For Landlords And Rental Property Owners Learn How Pay Less Taxe Rental Property Being A Landlord Colorado Rental

What Is Rental Property Depreciation

Understanding Depreciation Recapture When You Sell A Rental Property Millcreek Commercial Discover Freedom

10 Tax Deductions For Smart Investors Passive Real Estate Investing Real Estate Investing Flipping Real Estate Investor Real Estate Information

Flooring For Rental Properties All You Need To Know

Does Taking A Depreciation Of Rental Property Hurt Me When I Sell Home Guides Sf Gate

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcri5qjrbrig83skgl5 P6cpbid2ciogi8u8stevmfr4aarqijlt Usqp Cau

Source : pinterest.com